Laste ned presentasjonen

Presentasjon lastes. Vennligst vent

1

”Oljenæringens samfunnsansvar – et innlegg om holdninger, verdier og bedriftsfilosofi” Desemberkonferansen 2008 Gro Skaaren-Fystro, TI Norge gskaaren@online.no

2

Corruption Perception Index 2008 1Denmark9,36 1New Zealand9,36 1Sweden9,36 4Singapore9,29 5Finland9,06 5Switzerland9,06 7Iceland8,95 7Netherlands8,96 9Australia8,78 9Canada8,76 11Luxembourg8,36 12Austria8,16 12Hong Kong8,18 14Germany7,96 14Norway7,96

3

Hva skyldes fallet på årets indeks? Økt bevissthet om korrupsjon i Norge Det blir ikke gjort nok verken i offentlig eller privat sektor for å bøte på problemet

4

Examples of corruption in Norway Vannverksaken Oslo Kommune-saken Drammen Kommune-saken Gardermoen-saken Mannesmann/Statoil-saken UNICEF-saken Røde Kors-saken Statoil/Horton-saken Veritas-saken Ullevål-saken Finance Credit OVDS-saken SINTEF-saken Vinmonopolet Legeerklæringer Matvarekjedene Forsvaret Midtåsen-saken Båtsertifikat-saken Listen er mye lenger…..

5

Sectors most prone to bribery Public works/construction Arms and defence Oil and gas Real estate/property Telecoms Power generation/transmission Mining Source: TI Bribe Payers Index

6

PROMOTING REVENUE TRANSPARENCY

7

What is the Project about? Transparency can change resource curse in to a blessing Project Objectives: 1.To measure revenue transparency performance and diagnose areas for improvement. 2.To develop broad standards for revenue transparency. 3.To support the use of the revenue transparency standards and measures of performance by companies, rating agencies, investors, government regulators and civil society.

8

Companies Report Method Desk study Based on publicly available information Increased coverage: 42 companies in 21 countries of operation Indicators (framework): made adjustments to first one but kept comparability Addressed feedback from first iteration: context, refine questions, id N.A. Developed special SOE section Increased Anti-Corruption Participatory: early company engagement in Method refinement Data validation

9

Project Governance Reference ( Advisory ) Group Partners (TI,PWYP,RW) Industry Associations/Companies Governments Investors Rating Agencies EITI Secretariat Experts (industry, measurement, etc.) Working Group ( max 15 participants) TI Project Partners Measurement Experts Industry Associations of Company Reps / Governments Rep Country implementers EITI Secretariat Expert Task Forces for concrete tasks Project Management ADVICE MULTISTAKEHOLDER GUIDANCE MULTISTAKEHOLDER

Group Partners (TI,PWYP,RW) Industry Associations/Companies Governments Investors Rating Agencies EITI Secretariat Experts (industry, measurement, etc.) Working Group ( max 15 participants) TI Project Partners Measurement Experts Industry Associations of Company Reps / Governments Rep Country implementers EITI Secretariat Expert Task Forces for concrete tasks Project Management ADVICE MULTISTAKEHOLDER GUIDANCE MULTISTAKEHOLDER")

10

The questionnaire

11

Amerada Hess, Exxon Mobile, Chevron, Devon, Conoco Philips, Marathon Nexen, Talisman Petro Canada, Sonatrach Sonangol BHP Billiton, Woodside Petrobras Pedevesa CNPC, CNOOC, Petrochina, Sinopec SNP C Pemex GEPetro l Total ONG C Pertamina NIOC Eni Inpex Kazmunaingaz KPC Petrona s NNP C Statoil Gazprom, Rosneft, Lukoil Aramco Repsol Shell BP, BG Qatar COMPANIES REPORT 2007: COMPANY COVERAGE (per Home Country)

")

12

If comparissons were valid...

14

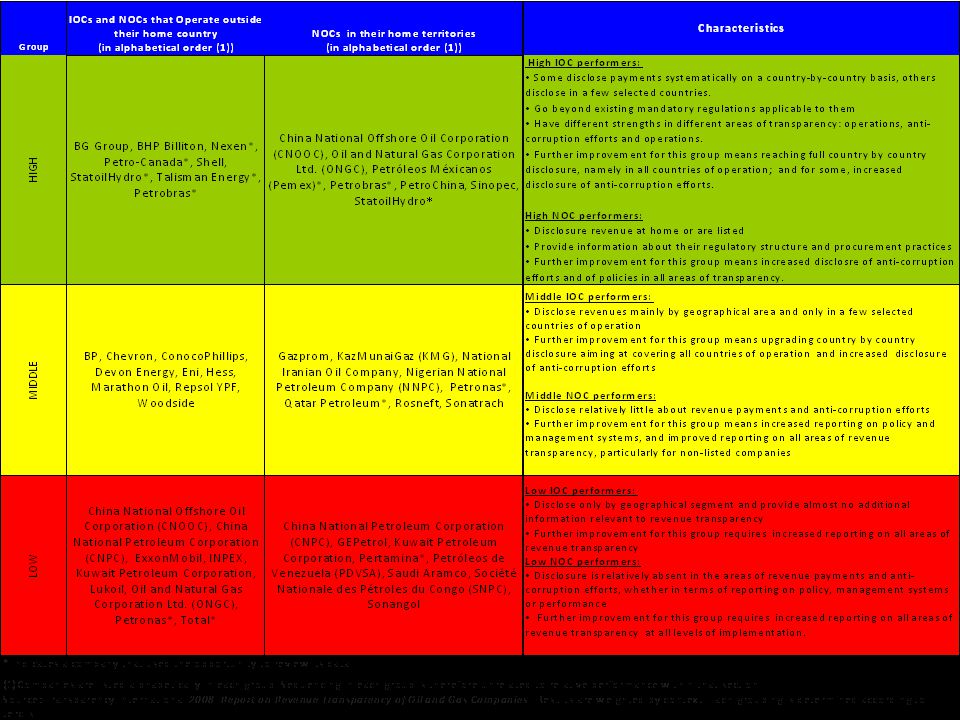

Policy Performance Poor performance disclosure Better performance than policy Better policy than performance Good policy and performance IOCs and NOCs outside their home jurisdictions Some policy, some performance Looking at our more detailed results and with respect to IOCs and NOCs outside their home jurisdictions, discrepancies are significant between public policy and actual performance disclosure…

15

Policy Performance NOCs home operations Good policy and performance Poor policy and performance Medium to good performance, irrespective of policy …whereas policy appears to matter less with NOCs operating at home.

16

Policy Performance IOCs and NOCs outside their home jurisdictions Based on our report, our long-term objective should be to move companies from official policy up to actual performance…

17

IOCs and NOCs outside their home jurisdictions Payments Operations …and to make disclosure of payments a standard element in disclosure of operations…

18

Recommendations Oil and gas companies should proactively report in all areas relevant to revenue transparency on a county-by-country basis. Home governments and appropriate regulatory agencies should require revenue transparency reporting for the operations of their companies at home and abroad. Governments from oil and gas producing countries should urgently introduce regulations that require all companies operating in their territories to make public all information relevant to revenue transparency. Regulatory agencies and companies should improve the accessibility, comprehensiveness and comparability of reporting on all areas of revenue transparency by adopting a uniform global reporting standard.

19

Challenges First integrated and systematic approach to companies: no body said it was easy. Creating and sustaining engagement with stakeholders is challenging: tradeoffs, courage, the meaning of collaborative approach. Delicate exercise of power balancing: keeping perspective, the meaning of multi-stakeholder approach; dynamics within the actors.

20

Extractive Industries Transparency Initiative (EITI) Lansert av Tony Blair i 2002 EITI fastsetter internasjonale og aktørspesifikke åpenhetsstandarder innenfor utvinnings- industrien Internasjonalt multi-stakeholder initiativ som involverer Betalere av inntekter (selskaper) Mottakere av inntekter (myndigheter) Brukere av informasjon (sivilsamfunnet) Giverland IMF, Verdensbanken, EBRD Investorer

Lansert av Tony Blair i 2002 EITI fastsetter internasjonale og aktørspesifikke åpenhetsstandarder innenfor utvinnings- industrien Internasjonalt multi-stakeholder initiativ som involverer Betalere av inntekter (selskaper) Mottakere av inntekter (myndigheter) Brukere av informasjon (sivilsamfunnet) Giverland IMF, Verdensbanken, EBRD Investorer")

21

EITI-kriteriene 1. Regulær publisering av alle materielle betalinger fra olje-, gass- og gruveselskaper til myndighetene og alle inntekter myndighetene mottar fra olje-, gass- og gruveselskaper. 2. Alle betalinger og inntekter (som nevnt over)skal være gjenstand for en kredibel og uavhengig revisjon hvor internasjonale regnskapsstandarder blir benyttet. 3. Betalinger og inntekter skal sammenstilles av en uavhengig administrator som benytter internasjonal regnskapsstandard. Administratorens konklusjoner skal publiseres.

skal være gjenstand for en kredibel og uavhengig revisjon hvor internasjonale regnskapsstandarder blir benyttet. 3. Betalinger og inntekter skal sammenstilles av en uavhengig administrator som benytter internasjonal regnskapsstandard. Administratorens konklusjoner skal publiseres..")

22

EITI-kriteriene 4. Kriteriene gjelder alle selskaper også statseide selskaper. 5. Det sivile samfunn skal være aktive som deltager i utformingen, overvåkningen og evalueringen av prosessen og skal også bidra i den offentlige debatten. 6. En offentlig og finansiell bærekraftig arbeidsplan for alle punkter nevnt over skal fremlegges av myndighetene. Arbeidsplanen skal inkludere målbare størrelser, en tidsplan for implementering og en vurdering av mulige kapasitetsbeskrankninger..

23

Business Principles for Countering Bribery Selskapet skal forby bestikkelser i alle former enten direkte eller indirekte. Selskapet skal iverksette et anti- korrupsjonsprogram.

24

Elementer i et anti- korrupsjonsprogram Gjøre ansatte kjent med relevante lovbestemmelser som gjelder for korrupsjon både hjemme og i aktuelle land Innfør etiske retningslinjer og følg opp med kurs og opplæring, Etabler internkontroller og rutiner for å avdekke uregelmessigheter Innfør et kontaktpunkt for varsling – gjerne eksternt Undersøk korrupsjonsrisiki i aktuelle markeder

Liknende presentasjoner

Turning customer feedback into appropriate actions and customer satisfaction.>")

>")